An investment thesis defined by Coeus Collective Ventures

Date

06/24/2026

Author

Antonio Di Meglio, Juhao (Leon) Li, Dahlia Mankovich

Executive Summary

The defining investment opportunity of the current decade is not artificial intelligence itself. Instead it is the infrastructure that makes AI tools economically useful at scale.

This paper presents a framework organized across five focus areas (Industrial Infrastructure, the Intelligence Layer, AI-Native Operating, Workflow Automation, Commercialization Infrastructure) and examines the historical precedent that gives the thesis its conviction.

These layers are interdependent, each one’s maturation expands the addressable market and productive capability of the others. Other categories may emerge or prove equally significant; the framework does not foreclose them. What it does is provide a coherent operating logic for evaluating if a company possesses platform-level defensibility.

SECTION I

Framing the Thesis

I.1

What is Infrastructure?

Few terms in economics and technology investing are used as frequently and defined as imprecisely as ˝infrastructure.˛ In common usage, the word conjures images of physical assets: highways, power grids, railroads, and ports. This physical intuition is not wrong, but it is incomplete.

The economist Brett Frischmann, in Infrastructure: The Social Value of Shared Resources (2012), offers the most rigorous demand-side definition available in academic literature. Frischmann defines infrastructure not by what it is made of, but by the role it plays: infrastructure resources are those whose value derives primarily from the downstream activities they enable, rather than from their direct consumption. A road, an internet backbone, and an enterprise software platform that governs how an entire industry operates are all infrastructure in the same meaningful sense. When they are removed, the productive capacity of those who depend on them is greatly diminished.

The distinguishing criterion is not hardware versus software. It is whether a system operates at the platform level whether it changes the rails on which an industry runs. The steam engine, the electric dynamo, and the internet each followed this pattern. Platform-level AI systems, robotics operating platforms, and workflow orchestration infrastructure meet the same criteria today.

I.2

What is the New Economy?

Don Tapscott introduced the term “new economy” in The Digital Economy: Promise and Peril in the Age of Networked Intelligence (1995), arguing that the digitization of information would fundamentally alter how value is created and distributed. That definition remains partially correct, but it is now insufficient. The “new economy” of the 1990s primarily moved information faster. The transformation underway today simultaneously re-wires physical production, organizational decision-making, and the execution of work itself across every sector of the economy. UNCTAD’s technical framework defines the new digital economy to explicitly include automated manufacturing, robotics, and artificial intelligence. The framework extends to, but is not limited to, deep technology verticals like quantum computing, photonics, biotechnology & life sciences, and advanced materials & clean technologies.

Prior technological transitions tended to restructure one domain at a time: the railroad reorganized distribution, electrification reorganized manufacturing, the internet reorganized information and communication. Each created generational investment opportunities precisely because the enabling infrastructure had to be built before the productive gains could materialize.

What distinguishes the current moment is that disruption is no longer confined to a single domain or industry; instead, it is concurrently restructuring how goods are made, decisions are reached, and markets are accessed.

What is equally important is that this transformation is not unfolding uniformly across industries. Instead it is advancing fastest and with the greatest economic consequence in the verticals where operational complexity is highest, data is richest, and the cost of inefficiency is most measurable. Manufacturing, logistics, financial services, healthcare, and enterprise software are not simply early adopters; they are the proving grounds where the new economy's operating infrastructure is being defined.

I.3

Why Infrastructure, Why Now?

The case for infrastructure investment at this moment rests on four converging signals: capital allocation, historical timing, enterprise adoption, and software-enhanced hardware.

Capital Allocation: AI firms captured 61% of all global venture capital in 2025 (up from 30% in 2022) representing $258.7 billion out of $427.1 billion in total VC deployed. McKinsey estimates that the global economy will require $106T in new infrastructure investment through 2040, and that the definition of infrastructure is expanding to include digital systems and AI-enabled assets alongside traditional physical categories.

Historical Timing:

Exhibits made by Coeus Collective Ventures. Data derived from third-party sources.

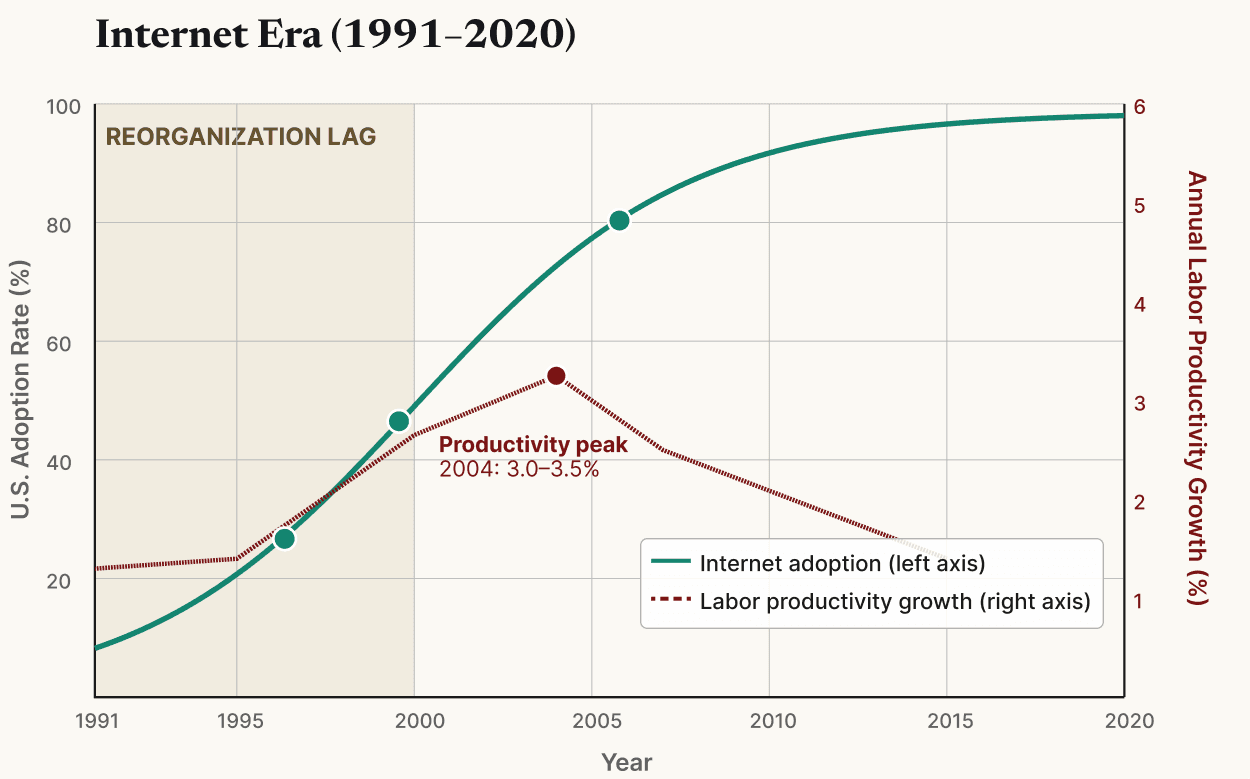

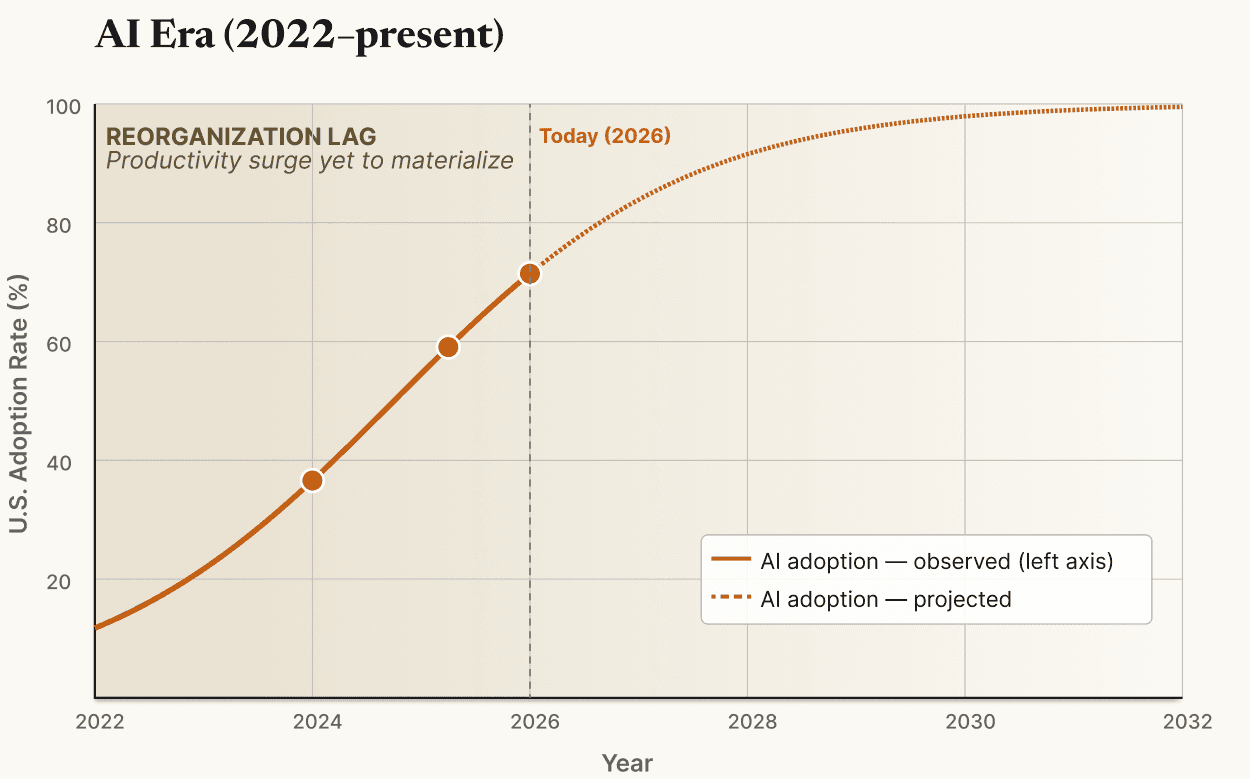

Electricity diffused across the U.S. economy for nearly four decades before aggregate productivity responded. Infrastructure investment creates economic value on a delayed schedule - a period Paul David coined as the reorganization lag. That period is when the infrastructure investment window is most compelling.

The internet compressed the reorganization lag to approximately nine years: adoption climbed steadily through the mid-1990s, but the productivity surge did not materialize until 2000–2004, peaking at 3.0–3.5% annual labor productivity growth as enterprises completed the operational restructuring that networked information enabled.

Generative AI has reached 50% U.S. adult adoption faster than any technology in recorded history, yet no corresponding productivity surge has appeared in aggregate statistics. The AI technology stack has crossed the threshold from experimental to deployable, making now the most attractive infrastructure investment entry point.

Enterprise Adoption: Enterprise investment in AI systems tripled in a single year (from $11.5 billion in 2024 to $37 billion in 2025). By 2025, the majority of AI spend had migrated into permanent operational budget lines: the category reserved for systems organizations depend on to function. This reclassification from innovation to operations is the standard organizational signal that a technology has graduated from exploratory to infrastructural.

Software-enhanced hardware: There has been a recent emergence of companies that combine proprietary hardware and AI software into a single integrated platform. This convergence is producing a category of infrastructure businesses with moat characteristics that neither pure software nor pure hardware companies can replicate independently. When a company controls both the data-generating physical layer and the intelligence layer that processes it, switching costs become organizational rather than contractual. The hardware embeds the software, and the software justifies the hardware. That integration is increasingly where platform-level moats in the new economy are being formed.

SECTION II

Focus Area Deep Dives

II.1

Industrial Infrastructure

Systems that modernize production, logistics, and the physical economy.

Industrial Infrastructure encompasses the technologies that rebuild how physical goods are made, moved, stored, and delivered. It includes robotics and warehouse automation, advanced manufacturing software, supply chain operating systems, industrial monitoring platforms, and logistics tools. What distinguishes these businesses as infrastructure rather than tools is their embedment in critical physical workflows: once integrated into the operating architecture of a factory, fulfillment center, or logistics network, they become part of the productive backbone.

The scale of the structural shift now underway is measurable:

The global industrial robotics market is projected to grow from $26.99 billion in 2024 to $235.28 billion by 2033, a compound annual growth rate of 27.2%.

More than 590,000 new industrial robots were installed globally in 2023, bringing the active installed stock to approximately 4.3 million units worldwide

Investment in humanoid and mobile robotics alone reached $7.3 billion in the first half of 2025, signaling that capital is moving well beyond traditional fixed-station automation.

Undergirding this is a generational shift in what robotics can do. The current generation is reprogrammable and sensor-driven, capable of operating across variable environments where prior generations required fixed configurations. That shift from mechanical speed to operational flexibility is what makes this moment structurally different from prior automation cycles. The most visible signal is the commercial deployment of humanoid and mobile robots.

CASE STUDY

Symbotic

Symbotic went public via SPAC in 2022 at an initial enterprise value of approximately $4.5 billion, reaching a peak market capitalization exceeding $14 billion — one of the fastest value-creation trajectories in industrial automation history. Its AI-powered robotic warehouse system now operates inside Walmart’s regional distribution centers, processing inventory at speeds reported to be up to 25 times faster than manual operations. The Symbotic platform is software-defined and continuously updated, meaning its value to customers compounds over time rather than depreciating with use. Once a distribution center’s architecture is built around Symbotic, replacing it requires re-engineering the entire facility.

II.2

Intelligence Layer

Systems that improve real-time decision-making inside workflows.

The Intelligence Layer comprises real-time systems that augment human decision-making by surfacing insights, recommendations, and risk signals within the workflows where decisions are made. What makes these systems infrastructure rather than analytics software is that they operate close enough to the decision that removing them reduces the speed, confidence, or quality of that decision at the moment it matters.

The cognitive science basis for this category is well-established. Daniel Kahneman’s foundational research in Thinking, Fast and Slow (2011) demonstrated that human judgment under conditions of complexity, time pressure, and information overload is systematically biased in predictable ways. The Intelligence Layer is the organizational infrastructure for correcting that structural limitation, not by removing humans from decisions, but by improving the informational conditions under which those decisions are made.

The market opportunity reflects this structural need:

The decision intelligence market is valued at $15 billion in 2024 and projected to exceed $36 billion by 2030 at a CAGR of 16.5%.

Augmented analytics – the broader category of AI and machine learning embedded in analytics workflows – is projected to grow from $13.62 billion in 2024 to $41.23 billion by 2029.

Organizations adopting decision intelligence platforms report decisions made five times faster than those relying on conventional BI infrastructure.

The current disruption moves intelligence inside the operating moment — embedded within the CRM, the EHR, the construction tool, or the financial planning system the operator already uses. Vertical systems are more defensible than horizontal ones because they are trained on domain-specific data that general-purpose models cannot match at sufficient depth.

CASE STUDY

Gong

A revenue intelligence platform that captures and analyzes sales conversations, surfacing real-time coaching, deal risk signals, and forecasting intelligence within existing revenue workflows. Gong reached a $7.25B valuation in 2021 and crossed $300M ARR; as of 2025 the company has documented enterprise deployment at Shopify, LinkedIn, and PayPal. Gong is a defining component of the Intelligence Layer because it did not compete on analytics dashboards — it embedded intelligence inside the call, the deal, and the pipeline workflow, making removal operationally painful for revenue teams that depend on it. The product does not report on sales; it shapes sales outcomes in real time.

II.3

AI-Native Operating

Systems where AI executes business processes directly.

AI-Native Operating describes the category where AI stops serving as a copilot and becomes the operator, executing end-to-end processes with limited human intervention. It encompasses autonomous back-office operations, AI-led customer service and support, end-to-end document and claims processing, and vertical AI systems that own outcomes in a defined workflow category.

The market projections for this category are staggering:

The Agentic AI market is valued at $7.84 billion in 2025 and projected to reach $52.62 billion by 2030, a CAGR of 46.3% (the fastest projected growth rate of any layer in this framework).

Vertical AI agents are projected at a CAGR of 62.7% between 2025 and 2030 (the highest-growth sub-segment within the category).

Bessemer Venture Partners reports that vertical AI companies founded post-2019 are reaching 80% of traditional SaaS contract values while growing 400% year over year.

Prior automation displaced routine, codifiable tasks while complementing non-routine cognitive work. AI-Native Operating extends the automation frontier into that previously protected cognitive domain (research, drafting, intake, qualification, customer engagement).

These are not productivity tools, they are operators of record for previously human-staffed processes. Vertical operators that own outcomes in a defined workflow category command higher enterprise budgets and accumulate proprietary process knowledge that resists displacement. The most differentiated companies in this category are already selling outcomes rather than software seats, and those that build governance and auditability into the operating architecture hold a structural advantage as AI controls tighten.

CASE STUDY

Sierra

Founded in 2023 by Bret Taylor (the former co-CEO of Salesforce and chairman of OpenAI's board) and Clay Bavor, Sierra is an AI-native customer service operating platform that resolves customer issues end-to-end without human handoff. The company raised $175 million in 2024 at a $4.5 billion valuation and is deployed at SiriusXM, Sonos, WeightWatchers, and Ramp, autonomously handling the full resolution workflow. Sierra is the clearest current case study for AI-Native Operating because the product does not assist a human agent. Instead it replaces the function entirely for defined categories of customer interaction, changing the labor model rather than improving it.

II.4

Workflow Automation

Systems that coordinate fragmented work into repeatable operating flows.

Workflow Automation encompasses platforms that transform manual, fragmented, cross-functional processes into coordinated, automated systems of execution. It includes workflow orchestration platforms, operational systems of record, approval and routing systems, and multi-stakeholder coordination tools. Workflow Automation governs the architecture that connects people, systems, approvals, and data into a repeatable operating structure. It is frequently the substrate layer on which AI-Native Operating systems run, making it infrastructure not only for human operations but for AI-agent ecosystems as well.

The category’s scale reflects its foundational position in enterprise architecture:

The workflow automation market is projected to grow from $26.01 billion in 2026 to $167.3 billion by 2032 at a CAGR of 26.7%.

Enterprise multi-agent architectures are now present in 72% of enterprise AI projects in 2025, up from 23% in 2024.

Gartner has placed hyperautomation on its Top Strategic Technology Trends list continuously since 2019, reflecting the category’s transition from emerging practice to enterprise standard.

The structural evolution of this category can be read as a series of expanding scope. The first generation replaced deterministic rule-based routing with configurable logic. The current generation replaces that with adaptive reasoning that handles exceptions, self-corrects without re-programming, and shifts configuration authority from engineering to operations owners. The third expansion, now underway, moves beyond orchestrating human steps into orchestrating multi-agent AI systems.

Workflow Automation platforms that have already built native AI orchestration capabilities are positioned to become the process backbone of AI-native enterprises.

CASE STUDY

Rippling

Founded in 2016, Rippling has built what may be the most complete demonstration of Workflow Automation as infrastructure: a single platform that coordinates HR, IT, and finance workflows across the full employee lifecycle. The company reached a $13.5B valuation in its 2024 Series F and now serves over 10,000 customers including Stripe, Superhuman, and Lightspeed. What makes Rippling a defining case study for this layer is not the breadth of its product surface but the structural consequence of its architecture: because it sits across every function that touches an employee, removal requires re-engineering the operating model of the entire organization rather than switching a single tool. Rippling's expansion trajectory, moving from HR into IT, then finance, then spend management, also demonstrates how Workflow Automation platforms extend their footprint once embedded.

II.5

Commercialization Infrastructure

Systems that make distribution, conversion, and revenue generation more scalable.

Commercialization Infrastructure comprises the systems that change how products reach markets, customers convert, revenue is captured, and GTM efforts scale. What makes these systems infrastructure rather than marketing tools is their embedment in the repeatable revenue engine.

There is a substantial performance gap between corporations’ current abilities and their potential that this category exists to close.

For a 50-person revenue team, GTM stack fragmentation costs between $800,000 and $1.4 million annually in direct tool spend, integration maintenance, and revenue lost to delayed signal response.

Companies with aligned revenue operations grow 12 to 15 times faster and are 34% more profitable than those with fragmented GTM functions.

The structural inefficiency is clear and is where the commercial opportunity lies. The market is shifting away from brute-force outreach and toward signal-based automation.

Precision Prospecting: Shifting from volume-driven outbound to signal-based AI that identifies high-probability buyers at their peak moment of intent.

Structural Efficiency: AI agents are replacing traditional SDR functions not just at the margin, but fundamentally. Vercel reduced its inbound sales development team from ten representatives to one after deploying AI GTM agents.

Consolidated ROI: CFOs now demand unified justification at renewal, forcing a transition from single-function tools to integrated platforms that span the entire revenue workflow.

CASE STUDY

Clay

An AI-native GTM data infrastructure platform that combines prospecting, enrichment, and outbound sequencing into a unified execution layer. Clay raised a $40M Series B in January 2024 at a $500M valuation and reportedly reached a $1.5B+ valuation in a 2025 round; its customers include Anthropic, OpenAI, and Notion. Clay demonstrates the Commercialization Infrastructure thesis at a particularly clear level: it does not sell a feature. What Clay does is it sells the rails on which modern GTM teams source, enrich, and convert pipeline, and its rapid revenue growth reflects how quickly this infrastructure has become operationally essential for AI-native revenue organizations.

SECTION III

Cross-Cutting Dynamics

III.1

Interdependencies Between Layers: The Compounding Thesis

The five categories in this framework are interdependent layers of a single operating architecture, and that interdependence creates a compounding dynamic that is as consequential for portfolio construction as it is for the companies operating within it.

AI-native enterprises that have built across integrated infrastructure categories already demonstrate 1.7x higher revenue growth and 3.6x greater total shareholder return than peers who have not. The most instructive evidence is the companies that deliberately span multiple layers.

Samsara began as Industrial Infrastructure (IoT sensors and telematics for physical fleets) and has expanded into the Intelligence Layer by converting that operational data into real-time driver coaching, predictive maintenance alerts, and workflow recommendations. The data flywheel runs in one direction: more physical assets generate more data, which improves the intelligence, which deepens the embedment.

Ramp sits at the intersection of AI-Native Operating and Commercialization Infrastructure, autonomously managing spend workflows while simultaneously powering the sales intelligence and GTM operations of its own revenue engine. The company reports that 80% of its sales workflows are AI-powered, making it both a builder and a buyer of the infrastructure it sells.

For a venture portfolio, this dynamic has a direct implication: a company embedded across two or more layers of the stack does not merely have a larger product surface, it has a structurally different moat. Switching costs are multiplicative rather than additive, because the cost of displacement scales with the number of layers the platform touches.

III.2

Risks and Counter-Thesis

Infrastructure investment at the inflection point of a general purpose technology transition does not arrive with settled answers on every front. Three structural uncertainties warrant direct examination.

Platform Capture: The most immediate structural risk is that hyperscalers (Microsoft, Google, Amazon, Salesforce) build across all five layers and bundle the resulting capabilities into existing enterprise relationships at pricing levels that new entrants cannot match. The defensible positions are vertical, outcome-linked, and workflow-embedded before horizontal equivalents reach maturity in the relevant industry.

Commoditization: A related risk is that rapid improvement of foundation models drives the intelligence and execution layers toward commodity economics. The counter-evidence is that commoditization risk is not uniform. Instead it is highest for undifferentiated horizontal products and lowest for companies with deep workflow embedment and and vertical domain specificity. As the cost of intelligence falls, the scarcity shifts to the proprietary data and infrastructure companies accumulate over time.

S-Curve Timing: Infrastructure investment is highest-conviction at the early acceleration phase of the technology S-curve — after proof of concept, but before mainstream saturation. The difference in the current cycle may be the compression of adoption timelines. AI has reached 50% enterprise penetration faster than any technology in recorded history, suggesting the lag between infrastructure deployment and productivity realization may be materially shorter than in prior transitions.

III.3

Moat Formation and the Infrastructure Premium

Infrastructure businesses derive their durability from three compounding mechanisms that distinguish them structurally from application-layer software.

The first is workflow embedment. When a platform is integrated across multiple teams, approval chains, and data flows, displacement requires re-engineering the operating model — not switching a contract. The cost of removal scales with depth of integration and, in mission-critical workflows, becomes effectively prohibitive regardless of competitive pricing pressure.

The second is the data flywheel. Infrastructure platforms generate proprietary operational data through the act of running workflows. That data improves the model, the improved model improves the product, and the improved product attracts more usage — a compounding loop that generic competitors cannot replicate without the underlying deployment base.

The third is domain specificity over time. As foundation models commoditize general intelligence, the scarcity shifts to context: the proprietary process knowledge, customer-specific configurations, and institutional adaptation that accumulate inside a deeply embedded platform. That context is not transferable to a new vendor.

Together, these mechanisms produce a revenue quality that application businesses structurally cannot match: infrastructure grows when customers grow, not when sales cycles close.

Conclusion

The evidence assembled across this paper converges on a single, durable conclusion: the global economy is in the early stages of a structural re-platforming, and the investment opportunity at the center of that transition is the enabling infrastructure that makes it possible. The five categories documented here (Industrial Infrastructure, the Intelligence Layer, AI-Native Operating, Workflow Automation, and Commercialization Infrastructure) are the clearest present expressions of the investment thesis.

The precise timing and sequencing of value realization across the stack will be answered in the coming years, but what this paper can establish and what the evidence does create is the structural case. General purpose technologies create their most durable investment returns during the reorganization period, before productivity gains are visible in aggregate statistics. Infrastructure businesses accumulate moats through mechanisms that compound rather than erode over time.

The capital allocation patterns of sovereign wealth funds, private equity, and enterprise operating budgets collectively signal an asset reclassification, not a technology cycle.

What the next iteration of this framework may include is already becoming visible. Hardware is re-entering the investment conversation with a force not seen since the semiconductor era (humanoid robotics, edge compute, and custom silicon) are making clear that the physical and digital layers of the stack are more interdependent than the software decade implied. Quantum computing represents a longer-horizon structural disruption that could fundamentally reshape the Intelligence and AI-Native Operating categories in ways not yet fully measurable. What will not change is the underlying logic: the investors who build durable positions in enabling architecture capture the returns that define a generation.

For questions or inquiries, please contact us at team@coeuscollective.xyz.